COUNTERPOINT TACTICAL INCOME SMA

Counterpoint Tactical Income SMA uses mean-variance portfolio optimization techniques to allocate to a diversified blend of passive and tactical funds across many asset classes. The strategy’s objective is to provide reasonable mid-high single-digit returns over the market cycle while keeping short term capital losses below the 5% level.

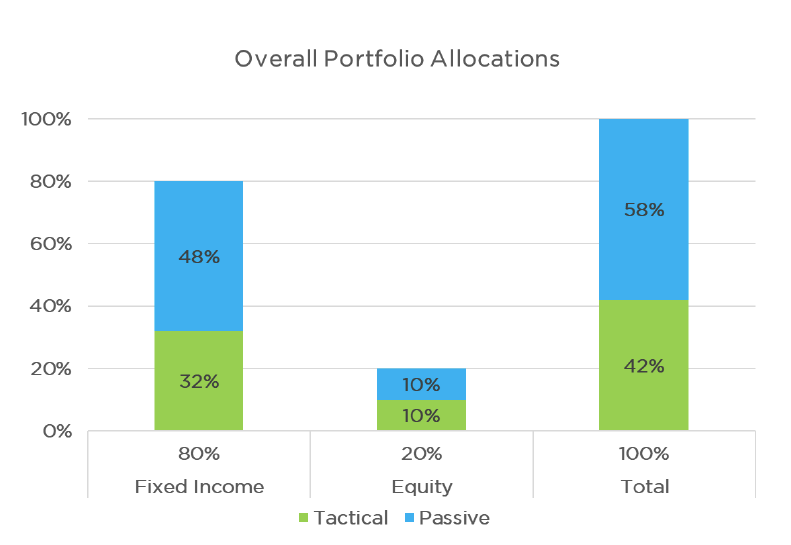

The strategy uses mutual funds advised by Counterpoint Mutual Funds as anchor holdings for approximately half of the total portfolio exposure to achieve its mandate. The model generally allocates across fixed income and equities with 80% and 20% of the portfolio exposure respectively, although these amounts may change from year to year as our model recalibrates risk expectations.

Portfolio Blend

We are invested in an optimal combination of tactical and passive mutual funds and ETFs to target reasonable return given an acceptable amount of risk.

Tactical – We access algorithmic trend-following signals within Counterpoint Mutual Funds’ Tactical funds. These signals determine if the fund should be entirely invested in either high yield bonds and equities or in treasuries and other lower risk securities.

Passive – In addition to tactical funds we own, we buy and hold a combination of fixed income, equity, and equity multi-factor funds that complement our tactical funds. This allows the portfolio to reduce performance drag at times when tactical strategies lag, seek outperformance through security selection, increase tax efficiency, and lower total portfolio expenses.

The above blend represents a typical model allocation in a given year, although these ratios may slightly shift year to year depending on our model’s decision.

Investment Process

The model considers the universe of liquid and investable broad asset classes, and performs an annually rebalanced mean-variance optimization to target lower turnover and increased tax-efficiency. In our testing, we have found intermediate-term mean-reversion effects within asset classes create an opportunity to increase the risk-reward tradeoffs of resulting allocations. Simply put, tilting return expectations upward for prior year underperforming asset classes enables the model to seek outperformance. The model will typically hold between 10-15 funds, representing a diverse selection of asset classes and strategies.

The model allocates to a balance of tactical, passive, and multi-factor alternative equity funds. Tactical holdings are meant to reduce portfolio losses in a turbulent market environment by switching from stocks or high yield bonds to safe-haven asset classes such as treasuries or cash. Multi-factor alternative equity funds are meant to seek outperformance by buying companies with positive attributes while selling short (which profits when their prices fall) companies with negative assets, as supported by academic research.

Combining the mean-variance optimization process with this alternatives investing framework provides a difficult-to-find objective framework in seeking the optimal combination of strategies with different risk-reward characteristics. By diversifying among these approaches, we believe an investor is better suited to thrive for the long-term through the stresses of many investment environments.

Counterpoint Asset Management, LLC is a California registered investment adviser. The firm only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice, but is limited to the dissemination of general information on products and services. Information presented is not an offer to buy or sell or a solicitation of any offer to buy or sell the securities mentioned herein.