COUNTERPOINT TACTICAL HIGH YIELD SMA

Counterpoint Tactical High Yield SMA uses systematic and quantitative trend following methods to seek the objective of providing meaningful income and exposure to recovery trends while keeping short term capital losses below the 5% level. The strategy seeks to own high yield bond funds in a stable or rising high yield bond market. In a falling high yield bond market, it seeks to own money market or low duration US Treasury funds.

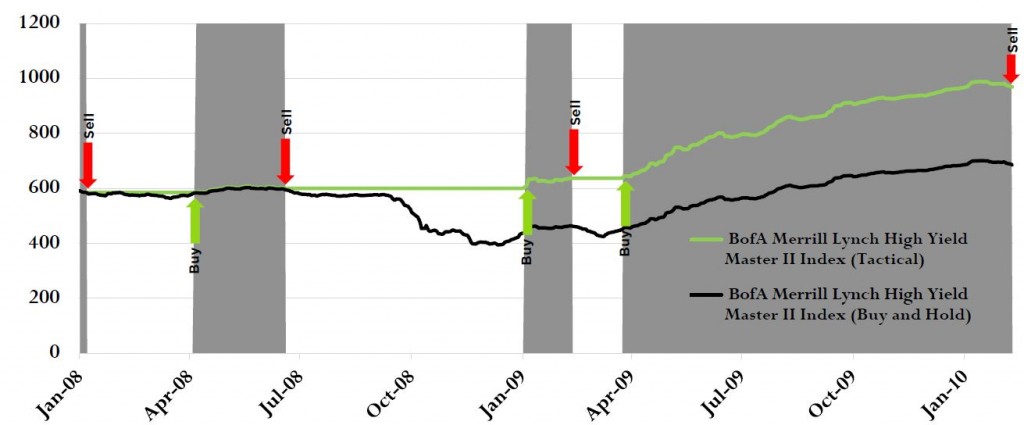

Tactical Versus Passive

The above depiction is not actual realized performance of the algorithm, but what the Tactical High Yield SMA algorithm would have signaled in this prior environment. The BofA Merrill Lynch High Yield Master II Index is a non-traded index reflecting the universe of US high yield corporate bonds with a maturity exceeding 18 months. Mutual funds and ETFs that track high yield benchmarks have often mimicked the movement of this index.

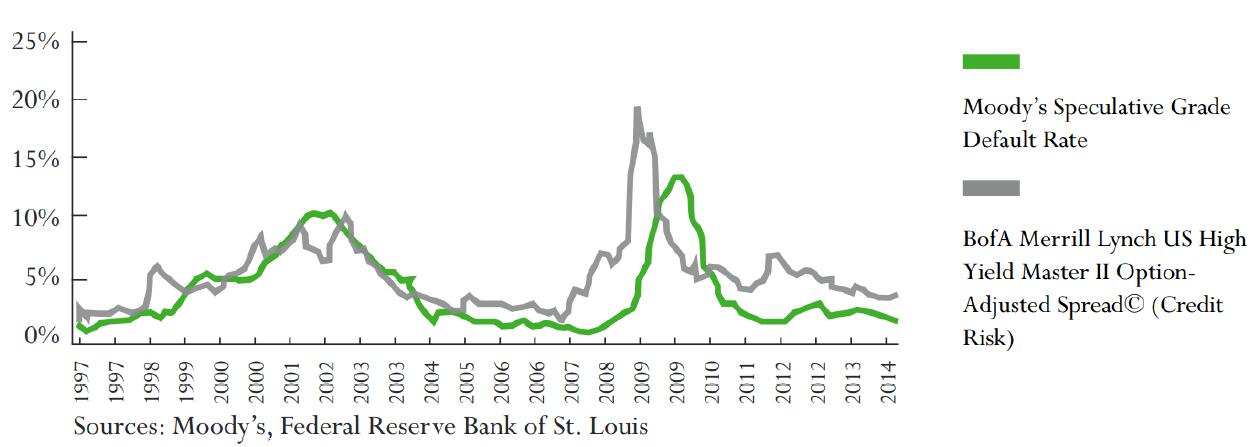

Drivers of High Yield Corporate Bond Prices

- Interest Rate Risk – the risk to a bond investment’s value from changes to economy-wide interest rates. Historical negative correlation to credit risks.

- Credit Risk – generally rises as the credit default cycle starts. This cycle plays out over many months in each direction and highly correlates with the price of credit risk.

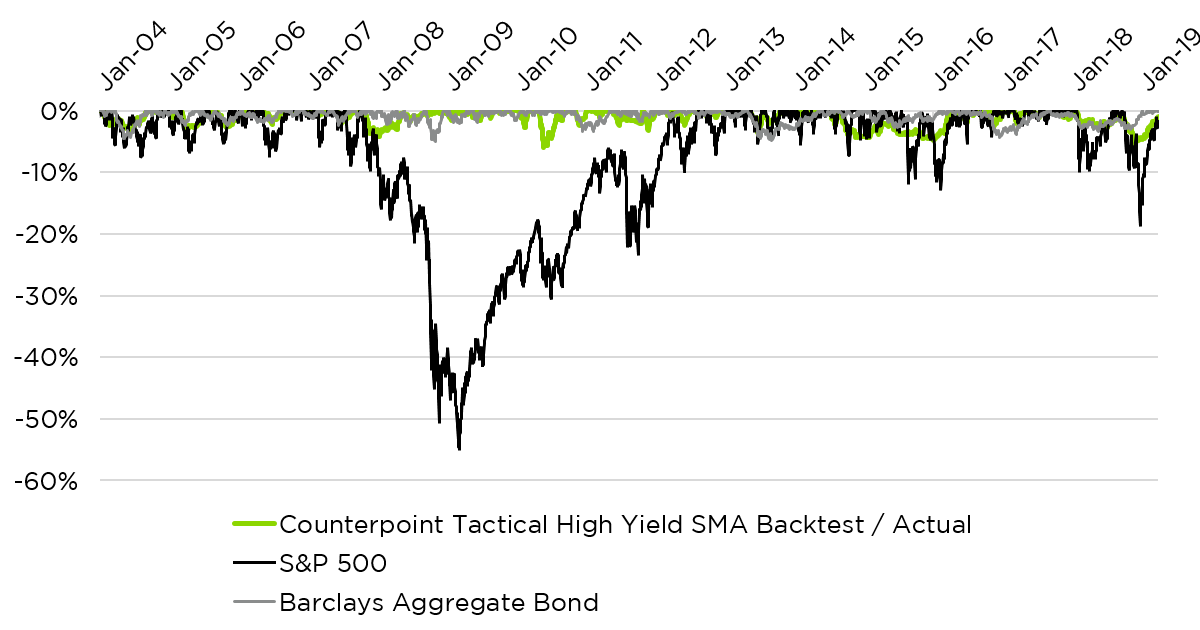

Drawdowns: Seeking A Winning Risk Profile

Counterpoint Asset Management, LLC is a California registered investment adviser. The firm only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice, but is limited to the dissemination of general information on products and services. Information presented is not an offer to buy or sell or a solicitation of any offer to buy or sell the securities mentioned herein.

Counterpoint Asset Management, LLC began offering the Tactical High Yield SMA in April of 2014, after the performance period depicted in the backtested results. Performance in this presentation reflects theoretical model results from January, 2004 until April, 2014. The model assumes a management fee of 2.0% and 0.5% in annual transaction costs to reflect a scenario of less than optimal execution. The backtest results were based on a randomized mutual fund selection within the high yield corporate bond sector. All results from May, 2014 to present are actual results of client accounts.

This presented past hypothetical and actual performance should not be construed as a predictor of future performance, for which there is a risk of loss. The backtest results do not represent the results of actual trading, but were achieved by a retroactive application of a model designed with the benefit of hindsight, and theoretically the strategy can continue to be tested and adjusted until better results are achieved. These backtest results all factor in the reinvestment of dividend income. Backtest results do not represent the impact that material economic and market factors might have on an investment adviser’s decision-making process if the adviser were actually managing client money. There are numerous factors related to the markets in general, many of which cannot be fully accounted for in the preparation of hypothetical performance results and all of which may adversely affect actual investment results.